Crude oil

Crude oil futures edged up ended more than 4% higher for October 2010 settled at $ 81.43. Crude oil prices traded in its known range of $75-$85 providing intraday traders to churn good profits with balanced economic data and ample supplies in product market. Oil prices traded in well mannered and remain fluctuated near $81 for the whole month on dollar fluctuations, mixed economic data and high inventory pressure.

The weaker dollar boost oil prices from the beginning of the month lifting above $80 on concerns over the second round of Quantitative Easing and stronger Euro. The increased import from China and positive economic data provide strength to oil prices to trade near $83. The record inventories in oil and product market on lower heating demand pressured oil prices to trade down near $81 for the remaining of the month discount to the ICE Brent.

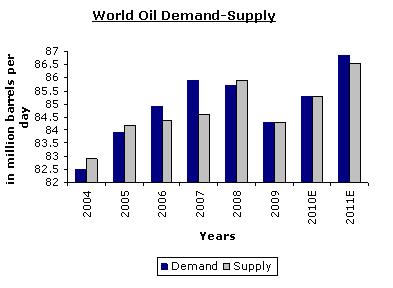

World oil demand supply balance is stabilizing with gradual economic recovery and increased demand for Non-OECD countries especially from China and India. The world oil demand is expected to rise to 86.37 mb/day in the fourth quarter of 2010 and 87.44 mb/day in 2011 while supplies to remain short to demand and expected to rise to 86.29 mb/d and 87.21 mb/d for 2010Q4 and 2011 respectively.

The stabilized economic recovery and increase in oil consumption was mostly supported by Govt aid and physical stimulus. However the emerging market counties have played significant role to balance the oil market with increased consumption. China’s economy has pushed the country’s oil demand up by more than 5.6%, which is almost half of total world oil demand growth. The consumption from India is expected to increase further with steady economic growth and increased new car registration which will boost demand for gasoline and diesel. Developing Countries’ oil demand growth is forecast to average 26.6 mb/d in 2010.

The moderate US driving season and neutral hurricane season has put huge pressure on crude oil and product inventories. Petroleum supplies are at the highest level in records since 20 years. Overall petroleum stockpiles including Crude oil and its climbed 8.92 mb to 1.14 billion, the highest level since at least 1990. The OECD industry stocks are at 61 days of forward cover levels above the 60 days of forward cover which reflects very bearish picture for crude oil market. However, the overhang in stocks, the high level of spare refining capacity and the floating storage is expected to remain unchanged for short term and will offset by increased oil demand.

The hurricane season so far has not affected the oil prices much compare to avg intense hurricane season. The hurricane season 2010 has generated 9 hurricanes and 10 tropical storms out of total 19 cyclone formations till date in Gulf of Mexico leaving oil and natural gas producing regions unaffected. The November season is not expected to generate much strong which may put pressure on oil prices for short term.

The prevailing economic uncertainty in world market and current situation in oil market is complicating the short term trend of crude oil prices. However the second round of QE will boost oil prices to trade near $90 but record storage will limit upside. OPEC has agreed to provide needed action to keep oil prices stable in case of dramatic hike. We expect oil prices to trade up in first half of November 2010 and than expected to remain stable with important resistance at $87 and with crucial support at $74.

Natural Gas

Natural gas futures rallied more than 6% gained for the second consecutive month settled at $4.04 for the month October 2010. The ample supplies and normal weather condition pressure natural gas prices to trade lower near $3.20 for the first three weeks of the month. The neutral hurricane season and lack of tropical storms also pressure prices as speculative positions declined on sufficient supplies. Natural gas prices got hit after NYMEX November contract expired in premium on wide contago backed by EIA inventory data showing lesser than expected storage build in spot market which lift natural gas prices above $4 in the end of the month.

Total Working gas in storage was 3754 Bcf as of Friday, October 22, 2010, according to EIA report. Stocks were 1 Bcf less than last year at this time and 312 Bcf, 9.10% above the 5-year average of 3442 Bcf. In the East Region, stocks were 69 Bcf above the 5-year average while stocks in the producing region were 193 Bcf above the 5-year average of 999 Bcf. The increased drilling activities on shale gas discoveries have put huge pressure on spot prices resulting in higher storage levels. At 3754 Bcf, total working gas is within the 5-year historical range. Inventories reached a record 3.837 trillion cubic feet last November.

The total world natural gas consumption is expected to increase by 1.60% to 111.5 Tcf/day for 2010. Total natural gas consumption in US is expected to rise by 4% to 65 Bcf/d in 2010. Projected consumption of natural gas for power generation grows by nearly 1.3 Bcf/d to 20.2 Bcf/d in 2010. The projected use of natural gas in the industrial sector also grows significantly in 2010, gaining by 6.4%, from 16.8 Bcf/d in 2009 to 17.9 Bcf/d in 2010. The increased dependability on natural gas to reduce greenhouse gases compare to other alternatives will boost natural gas consumption resulting in increasing in prices.

U.S. gas production rose 1.6% in August as output from wells in the Gulf of Mexico and Louisiana increased. Output increased to 72.38 bcf from a revised figure of 71.27 bcf in July 2010. EIA expects total marketed natural gas production to decline by 1.50% in 2011. Natural gas production grew steadily for the first half of the year on increased shale gas drilling activities. The total number of working natural gas rigs increased to 967 from 751 in December 2009 due to higher prices. A total of 7.9 Bcf of natural gas production was shut in because of hurricanes during June, July, and August. Based on the latest NOAA hurricane forecast, the production shut include 66.3 Bcf during the final 3 months of the hurricane season.

Natural gas spot prices increase in the end days of the month October 2010 on cooler temperatures. Residential and commercial consumption, increased approximately 2.2 Bcf per day in the last week of the month as cooler temperatures entered the northern parts of the country. About 52% of U.S. households use natural gas for heating. However whole sale natural gas prices at the bench mark Henry Hub delivery point fell almost 13% on lower demand for the throughout the month near $3.35 from $3.86 of previous month. EIA expects the annual average natural gas Henry Hub spot price for 2011 to be $4.58 per Mcf reporting decline against prior forecast.

The hurricane season is about to end and which has not affected much to the producing region so far on lack of stronger storms. The demand for natural gas will remain low for the short term until cold waves knock on the doors. However the forecasts for cooler weather have started and below-average temperatures are expected along the U.S. East Coast and parts of the Gulf of Mexico coast from Nov. 3 through Nov. 7, according to Commodity Weather Group. The stockiest will buy natural gas now before real demand get rise to take price advantage.

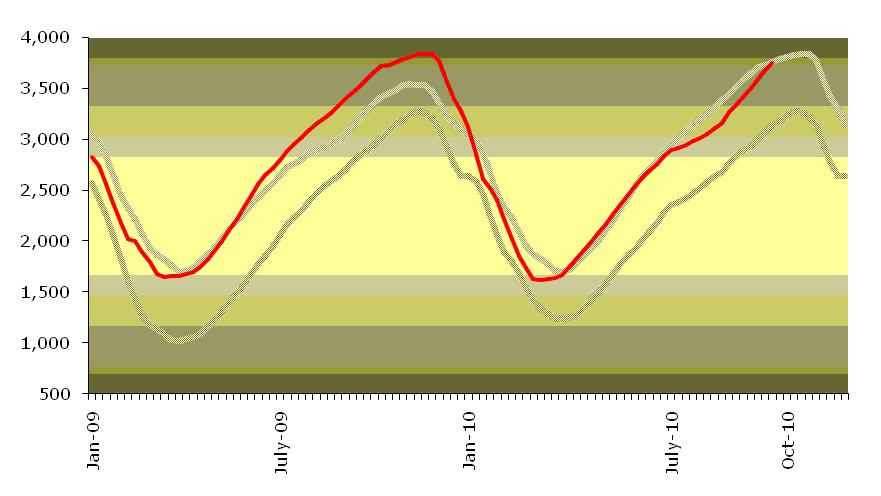

NYMEX Natural Gas

We expect natural gas prices to trade higher after a correction in the first half of the month discounting the premium to the November expiry supported by increased cooling demand. The industrial outlook seems positive and demand from industries will grow with gradual economic recovery. We recommend buying on dips in natural gas with important resistance at $5.10 with support at $3.10.